TL;DR: Insuring a bespoke classic Land Rover Defender requires an Agreed Value (or Guaranteed Value) policy from a specialty collector carrier like Hagerty or Grundy. Expect to pay between $1,200 and $2,800 annually in 2026 for a custom build valued north of $150,000, provided you meet strict garaging and daily-driver requirements.

Three years ago, a client called me from the side of a Texas highway. His custom 1997 Defender 90—a truck we had spent fourteen months stripping to the bare metal, hot-dip galvanizing, and outfitting with a 430-horsepower GM LS3—was sitting in a ditch. A distracted driver in a rented sedan had clipped his rear quarter panel at fifty miles an hour. He was fine. The truck was crushed.

Then the claims adjuster showed up. The representative looked at the VIN, punched it into a standard corporate database, and offered our client $24,000.

This is the catastrophic reality of standard auto insurance. They look at your paperwork and see a thirty-year-old farm implement. They absolutely do not see the modernized drivetrain, the heavy-duty suspension, or the hundreds of hours of labor required to achieve Concours-level fit and finish. If you bring a bespoke commission to a standard carrier, you are asking to lose six figures in the event of a total loss.

I have personally overseen more than 150 ground-up Defender builds. I know exactly how much blood, sweat, and capital goes into these trucks. You need specialized coverage that respects the machinery.

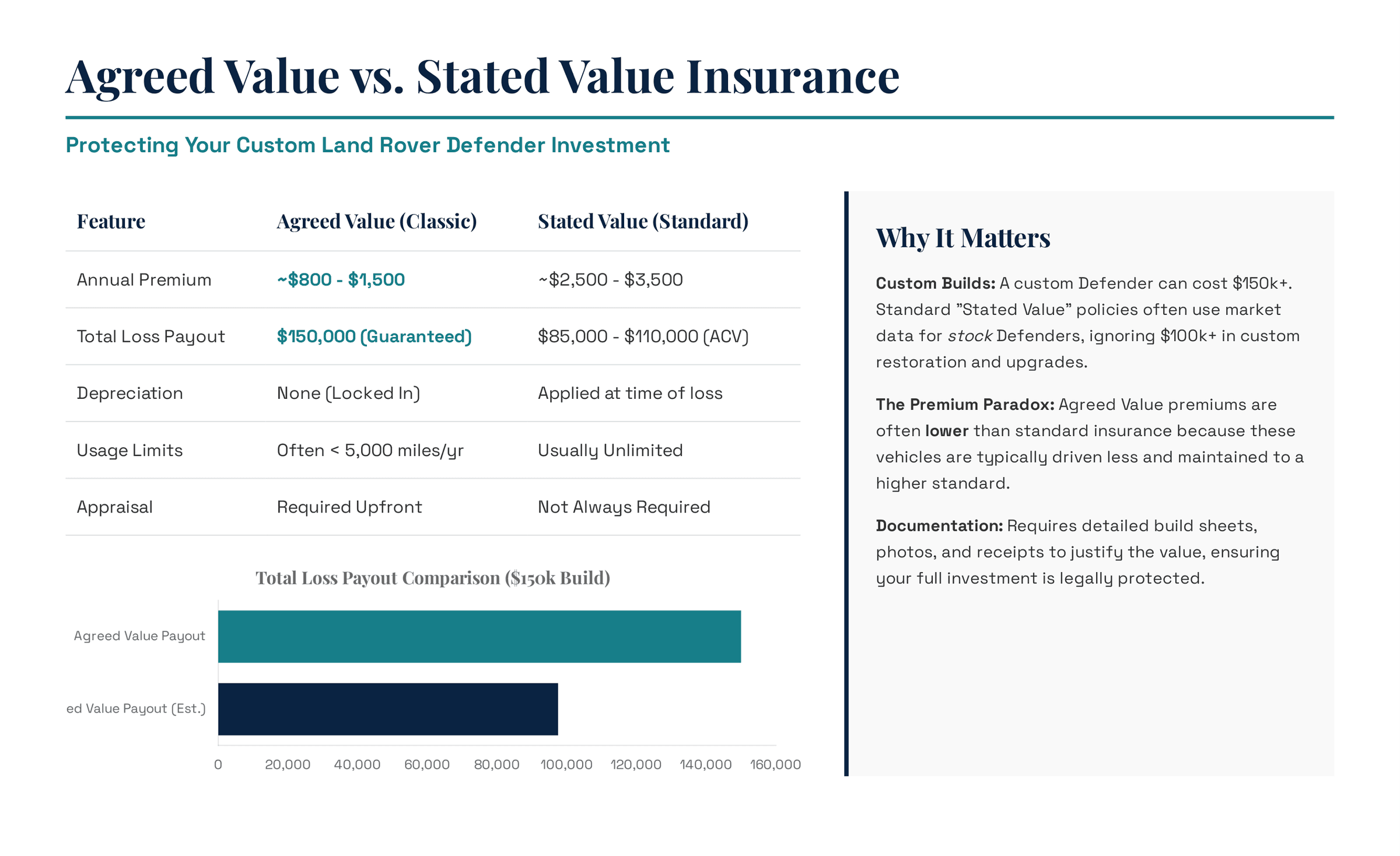

The Trap of Standard Insurance Policies

A standard auto policy will financially ruin you if your custom classic Defender is totaled. Regular carriers use Actual Cash Value formulas that heavily depreciate classic vehicles based on their age. You must avoid standard policies and completely avoid any contract offering "Stated Value" instead of a firm guarantee.

There are three types of insurance payout models, and two of them are useless to a collector.

Actual Cash Value (ACV) is what you have on your daily driver. The moment you leave the lot, the vehicle depreciates. If you wreck an ACV-insured 1996 Defender 110, the adjuster calculates what a used, rust-bucket 1996 Defender is worth on the local scrap market. The payout will not even cover the cost of the custom-mixed paint we use in our shop.

Then you have Stated Value. I despise Stated Value policies. Insurance agents often sell this to classic car owners by telling them they can "state" what the vehicle is worth upfront. The premium is calculated based on that high number. You feel protected. But read the fine print. A Stated Value policy allows the insurer to pay the stated amount or the Actual Cash Value, whichever is lower. They will always choose the lower number. It is a one-way street designed to maximize their premium collection while minimizing their risk.

Agreed Value: The Only Acceptable Coverage

Agreed Value policies guarantee a specific payout amount in the event of a total loss with zero depreciation. You and the underwriter legally establish the vehicle's exact worth before the policy is signed. If the worst happens, you receive a check for that exact dollar amount.

Hagerty calls this "Guaranteed Value," while other carriers stick to the traditional "Agreed Value" nomenclature. Whatever the marketing department calls it, the mechanics are the same. You prove the value of the vehicle through build sheets, invoices, and professional appraisals. The insurer reviews the documentation. You both sign off.

This is where documenting our 12-stage manufacturing process becomes critical for our clients. We provide exhaustive build sheets detailing the exact specifications of the commission. When an underwriter sees a factory-fresh GM LT1 pushing 460 horsepower and 465 lb-ft of torque mated to a heavy-duty 6L80E transmission, the valuation makes sense. We hand them the paperwork. They stamp the approval. Look through our projects portfolio, and you will see exactly the caliber of engineering that makes these six-figure valuations undeniable to specialty carriers.

What Does It Cost to Insure a Custom Defender in 2026?

Expect to pay between $1,200 and $2,800 annually to insure a six-figure bespoke Land Rover Defender in 2026. Your exact premium depends heavily on the agreed value amount, your chosen specialty carrier, garaging conditions, and your zip code. A flawless driving record is strictly mandatory.

Recent Bring a Trailer auction data paints a clear picture of the current market. In late 2024 and 2025, LS-swapped classic Defenders regularly hammered between $86,000 and $118,000 for standard refurbishments. Hagerty’s 2026 valuation tool places a stock, unmodified 1997 Defender 90 NAS in excellent condition at $105,000.

A true ground-up Monarch commission commands significantly more than a standard auction refurbishment. When you are insuring a truck for $200,000, your annual premium will scale accordingly. Yet, specialty insurance is remarkably inexpensive compared to insuring a modern supercar of the exact same value. Why? Because underwriters know collectors treat these vehicles like heirlooms. You are not taking your hand-stitched Italian leather interior to the grocery store during a hail storm.

Top Specialty Insurance Carriers for Land Rovers

The best carriers for a custom Defender are Hagerty, Grundy, and American Collectors Insurance. These underwriters exclusively specialize in classic and modified vehicles. They understand the collector market, offer true Agreed Value policies, and provide in-house parts specialists.

Hagerty

Hagerty remains the gold standard in this industry. They are not the cheapest. They are the best. If you need a replacement pane of Alpine glass or a highly specific wiring use, their claims department actually knows what you are talking about. Hagerty also offers a brilliant provision called "Cherished Salvage." If your Defender is involved in a devastating fire and they declare it a total loss, they pay you the full Agreed Value. But you get to keep the scorched chassis and salvageable parts. For a builder, that is massive.

Grundy

Grundy is historically more affordable. A $150,000 build might quote hundreds of dollars cheaper per year through Grundy than Hagerty. They offer zero-deductible options and unlimited mileage for pleasure driving. The tradeoff is rigidity. Grundy is notoriously strict about their usage requirements. If they find out you drove the Defender to work on a Tuesday just because the weather was nice, and someone rear-ends you in the company parking lot, they can deny the claim.

American Modern

If you are buying a truck from our inventory or commissioning a fresh build, American Modern is excellent for covering vehicles under active restoration. They offer up to $2,000 in spare parts coverage out of the gate.

The Rules of the Game: Red Flags and Requirements

Specialty carriers require you to own a daily driver insured with a standard auto policy. You must also prove the classic Defender is stored in a fully enclosed, locked garage. Carports and driveway tarps will instantly disqualify you from coverage.

These companies offer low rates because their risk exposure is mathematically tiny. They know the truck is sitting in a climate-controlled bay 90% of the time.

You must be prepared to prove this. Insurers will ask for photos of the garage interior. They will verify the standard insurance policy on your daily driver. They will check if the daily driver is appropriate for your commute. If your daily driver is a two-seat Mazda Miata and you live in snowy Michigan, the underwriter might suspect you plan to use the heavy-duty, LS3-powered 4x4 Defender as your actual winter commuter. They will reject the application.

Mileage restrictions vary wildly. Hagerty generally offers flexible "occasional pleasure use" with no hard numerical limit, so long as the spirit of the rule is followed. Others cap you at 2,500 miles a year. Know your contract.

Proving the Value of a 13-Stage Bespoke Commission

You cannot just tell an underwriter that a truck is fast and expect a $200,000 policy. You must provide a highly detailed itemization of the modernization process, including chassis renewal, engine integration specs, paint codes, and interior material costs.

When a client initiates a build with us, we supply an exhaustive dossier. The Defender market is full of cheap fiberglass body kits bolted onto rotting 1980s frames. Underwriters are deeply suspicious of "restored" Defenders without proper provenance.

We hand them the proof. We show the bare metal teardown. We document the hot-dip galvanized chassis—which permanently eliminates the catastrophic rust issues that plagued the original British factory run. We detail the modern damping technology in the suspension, the heavy-duty axles, and the proprietary wiring use required to make a modern GM V8 communicate with classic analog gauges. We outline the labor hours spent achieving perfect panel gaps on aluminum skins that left the Solihull factory looking wavy thirty years ago.

Read more about our obsessive engineering standards on our about page. When underwriters see Monarch Defender on the invoice, the Agreed Value negotiation is over before it begins.

Protecting Your Investment Before Delivery

Builders require milestone payments during a 14-to-18 month commission. You must insure your financial stake in the vehicle while it is still in pieces on the shop floor. Ask your specialty carrier about "Restoration in Progress" coverage.

Standard shop insurance covers the facility, but you want your own protective layer over your specific asset. This is a conversation you need to have with your Hagerty or Grundy agent the moment you sign a build contract.

I tell every client the exact same thing on day one. Building a bespoke Defender 90, 110, or 130 is an exercise in legacy. You are creating a mechanical heirloom. You do not cheap out on the foundation, you do not compromise on the powertrain, and you absolutely do not leave the financial protection to an algorithm at a discount insurance firm.

The 2007 Td5 engine made 122 horsepower. Which sounds perfectly adequate until you are trying to merge onto an interstate with a loaded roof rack—the engine screams at 3,800 RPM and you are barely breaking fifty miles per hour. That era is dead. We build trucks that pull from 2,000 RPM in third gear on a gravel road with terrifying, beautiful authority. You need an insurance policy that respects what that machine can do.

If you want to read more about the differences between specific eras and engines, browse our /blog. The history of this platform dictates how it is valued today.

Start Your Commission

We do not repair old trucks. We do not sell parts. We engineer the finest classic Land Rover Defenders on earth from the ground up. Our 12-stage bespoke manufacturing process strips the original classic down to its bare essence before rebuilding it with galvanized armor, high-performance GM V8 power, and handcrafted luxury.

If you are ready to command a vehicle built entirely to your exact specification—and you now know exactly how to protect it—it is time to talk. Visit our /contact page to begin your Monarch Defender commission.